Don’t let Trump tweets fool you. The oil price war is just starting.

Apr 4

2020

Don’t let Trump tweets fool you. The oil price war is just starting.

Small business is supposed to start getting help Friday. Will they?

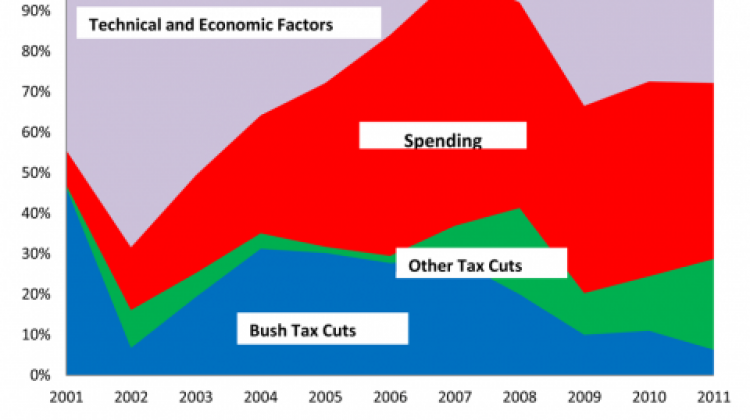

Guess which way it’s getting redistributed under the GOP tax scam.

While Donald Trump was making promises, the rest of the country was ignoring him.

Nearly 15,000 jobs will soon be lost in North America, with our country taking the biggest hit.

Tis' the season. Gifts exchanged, drunken parties, family, friends, oh and the annual dispute between networks and carriers. The most interesting one of this season is happning right now.

A new acquisition is announced today, continuing a troubling streak that is going to put our economy in even more risk.

Mozilla, on the heals of their botched hiring of Brendan Eich as CEO, is now fighting the recent FCC decision to allowed a tiered internet. The companies plan is powerful and it just might work.

People talk about income inequality all the time, but a new report shows that it is very equally distributed – amongst the top 85 richest people in the world

This has to be one of the most idiotic things I have read in ages. Shouldn’t be shocking, coming from a former Bush writer: Barring a last-minute breakthrough, taxes will go up for every U.S. taxpayer on Jan. 1 — and that’s a development conservatives should welcome. Don’t get me wrong: It would be better […]